North American Agronomy M&A: 2025 Review and Outlook

March 19, 2026 | By Ocean Park

2025 NORTH AMERICAN AGRONOMY M&A REVIEW

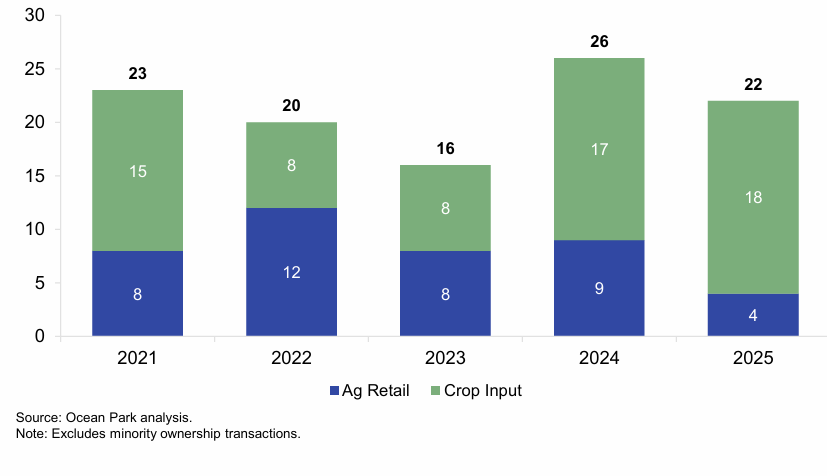

The agronomy market, comprised of ag retail and crop input companies, recorded another busy year of M&A activity, consisting of four ag retail deals, 18 crop input deals and several investments by the publicly-traded companies in the sector. Prior headwinds facing the industry remained in place, such as depressed commodity prices, pressure on farm incomes, tight margins and inflationary operating costs. For 2025, the volatility of trade policy and tariff levels added to uncertainty. Our view is this environment will continue to compel owners and managers in the sector to consider consolidation to gain efficiency, exits for family owners and investments to supplement research budgets.

North American Agronomy M&A Transactions, 2021-2025

AG RETAIL M&A

After nine deals in 2024, only four closed in 2025. Last year we outlined the key industry dynamics driving M&A transactions (namely, increased gross margin pressure, inflationary operating expenses, lack of succession plans, operational consolidation, and geographic expansion). These forces are still in play.

In addition to the transactions that closed, several cooperatives announced that they were exploring or actively in the process of merging with or acquiring other regional cooperatives.

- CFS and Ag Partners merger talks initiated and since terminated.

- Mercer Landmark, Sunrise Cooperative, Centerra Cooperative merger talks ongoing.

- Premier Companies and Superior Ag merger talks initiated, with an undisclosed outcome.

- Ag Plus and Farmward Cooperative announced plans to merge, with process ongoing.

The consolidation of cooperatives is a well-established trend, highlighting the push to gain scale and efficiencies.

Midwest agricultural cooperative consolidation is being driven primarily by shrinking profits in retail agronomy, rising capital and technology requirements, and growing balance sheet risk. Aging management teams and overlapping trade territories are accelerating local-to-local mergers, while larger regional cooperatives are leveraging scale to spread technology investments and strengthen risk management. As producer expectations shift toward full-service agronomy and digital integration, sub-scale cooperatives face increasing pressure to merge.

Only one private, independent deal closed in 2025 though we are aware of half dozen transactions that were in play. Deals involving small, independent ag retailers can easily take longer than six months to close given the small management teams who juggle customer needs with corporate transactions. The Arthur Companies unsuccessfully competed with CHS for West Central in 2024. However, they successfully closed on two smaller acquisitions in 2025. We expect them to continue their acquisition strategy.

As a reminder, these were only the publicly-disclosed ag retail transactions. Many ag retail deals are never disclosed.

The national players in North America – Helena and Nutrien – continue to actively review acquisitions to expand or fill-in their networks. On the other hand, Simplot is shifting their focus towards consolidating locations and building larger hubs. They are less likely to look at acquiring smaller ag retail locations. Wilbur-Ellis has cut back on acquisitions. They sold their animal nutrition business and completed a major refinancing last year.

Ag Retail M&A Transactions

Transaction Details:

- Northwest Grain Growers (NWGG) and Mid-Columbia Producers (MCP) merged.

Two Pacific Northwest cooperatives, Northwest Grain Growers and Mid-Columbia Producers merged in May. The merger combines NWGG’s grain marketing, grain storage and seed operations with MCP’s grain marketing, grain storage, propane, agronomy services and farm supply store operations. The combined entity, operating under Northwest Grain Growers with 2,900 members, has 65 grain facilities and eight seed facilities across Washington and Oregon. Two Nebraska-based cooperatives, Panhandle and FCE, merged to form Legacy Cooperative. The combined entity will operate nine agronomy locations with eight in Nebraska and one in Wyoming, serving farmers across Nebraska, Wyoming, South Dakota, and Colorado.

- Aurora Cooperative and Farmers Union Cooperative merged.

Two Nebraska-based cooperatives, Aurora Cooperative and Farmers Union Cooperative merged in September. The combined entity will offer crop protection, crop nutrition, seed, animal feed, energy products and grain services across its 73 locations.

- The Arthur Companies acquired AgriMax.

The Arthur Companies, a grain and agronomy business with operations in North Dakota and Idaho, acquired AgriMax, an independent ag retailer in Minnesota. The acquisition expands Arthur Companies’ agronomy offerings and extends its grower base into Minnesota’s Red River Valley, adding AgriMax’s locations in Fisher and Fertile to its six existing North Dakota agronomy locations.

- The Arthur Companies acquired Right Way Ag Aerial Spraying.

The Arthur Companies made a second purchase in 2025, acquiring North Dakota-based Right Way Ag. The Arthur Companies integrated Right Way Ag’s aerial application services with AgriMax’s agricultural retail operations, creating a differentiated service offering for North Dakota and Minnesota growers.

CROP INPUT M&A

In the crop input sector, which includes the distribution and production of seeds, biologicals, crop nutrition, crop protection, and other essential inputs, we tracked 18 deals in 2025 versus 17 deals in 2024.

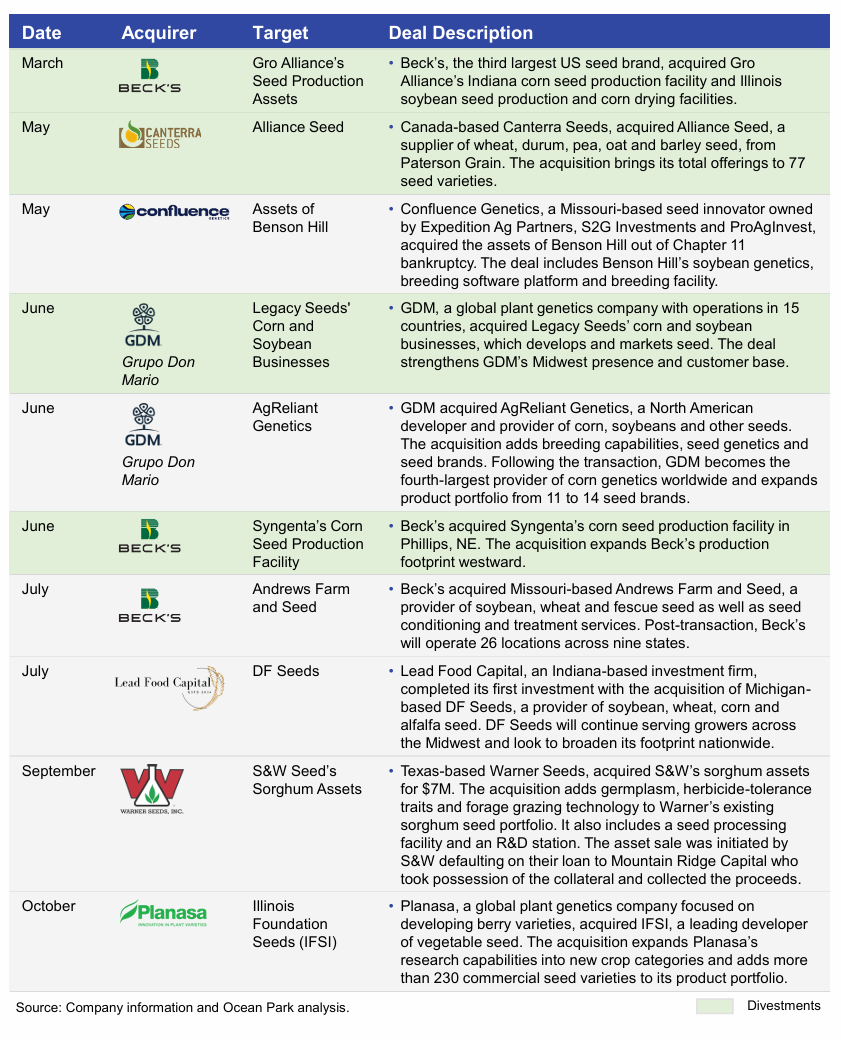

The deal themes in 2025 were no surprise: divestments, the seed value chain (genetics, production and distribution), biologicals and private equity participation. Larger companies pruned non-core businesses. The seed sector continued its consolidation, with ten transactions centered on expanding production capacity, broadening product portfolios, strengthening R&D capabilities, acquiring proprietary genetics and extending geographic reach. The acquisitions underscored a sector pursuing scale, integration and differentiated technology. Biological companies with larger distribution capabilities acquired smaller biological companies that reach critical mass to strengthen their product offerings and capabilities. HGS BioScience illustrated this dynamic through a series of acquisitions that expanded access to raw materials, increased processing capacity, broadened its product portfolio and enhanced R&D capabilities. Private equity involvement continued, with several PE firms and PE backed platforms acquiring crop input manufacturers and providers, reinforcing their role as consolidators and growth accelerators in the industry. These reasons underlay every deal in 2025.

Millborn Seeds and The NativeSeed Group who were active in 2024 but quiet in 2025, likely focusing on integrating the multiple deals each closed in 2024.

Seed M&A Transactions

CROP INPUT M&A – BIOLOGICALS

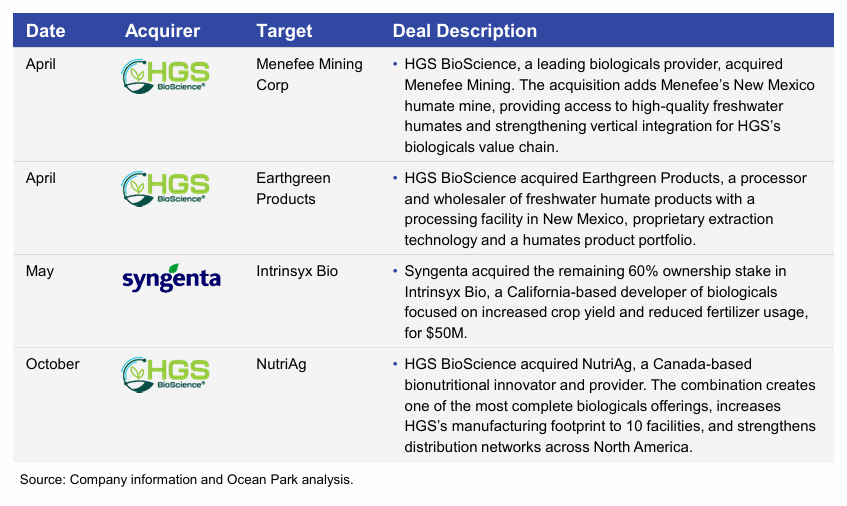

At four transactions, biologicals was an M&A focus in 2025 with HGS BioScience, backed by Paine Schwartz, an agribusiness-focused private equity firm, building its portfolio to 13 biologicals products through acquisitions and Syngenta acquiring a stake in a California-based biological company.

Biologicals M&A Transactions

CROP INPUT M&A – CROP PROTECTION AND NUTRITION

Other M&A transactions in crop inputs featured four transactions in the crop protection/nutrition space, with two of the four acquirers being private equity firms.

Crop Protection and Nutrition M&A Transactions

CROP INPUT INVESTMENTS BY THE MAJOR PUBLICLY-TRADED COMPANIES

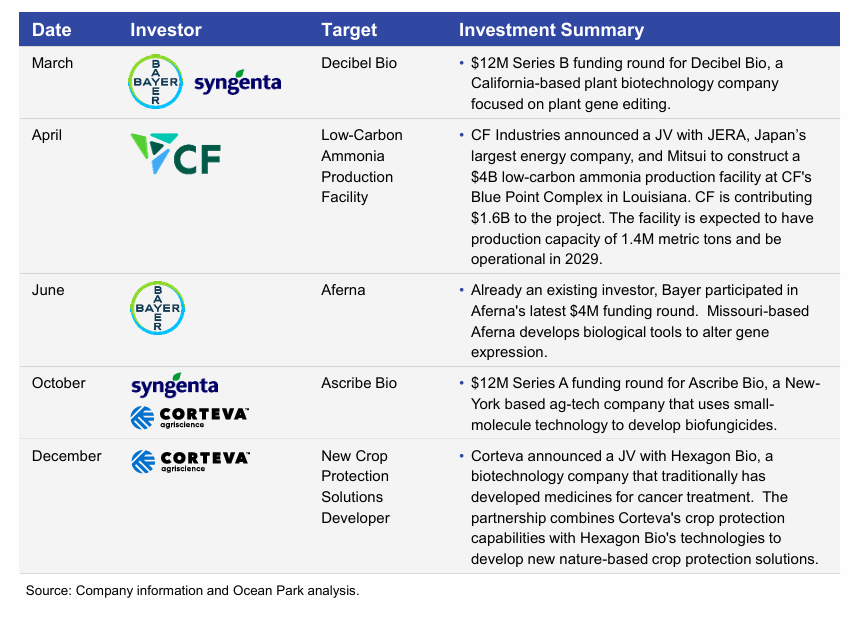

In 2025, large corporations continued to invest in small venture rounds and joint ventures in what amounted to a relatively quiet year. Bayer, Syngenta, and Corteva each made investments into ag technology/biotechnology companies to supplement their own R&D and product pipelines.

Crop Input Public Company Investment Deals

CORPORATE TRANSFORMATIONS

2025 was marked by significant corporate transformations within the agricultural and crop input sector, most notably the announced separation of Corteva and the ongoing spin-off by BASF. Together, these actions reflect a broader industry trend toward increased specialization, operational efficiency, and strategic realignment.

-

- Corteva Separation.

Corteva announced plans in October 2025 to separate its crop protection and seed business into independent publicly-traded companies. New Corteva will comprise the crop protection segment, with a focus on biologicals and “green chemistry” businesses. SpinCo will comprise the seed business, centered on advancing genetics and proprietary traits. Estimated 2025 net sales are $7.8B for New Corteva and $9.9B for SpinCo. Corteva hopes the spin-off will unlock value by allowing each business to tailor its own capital allocation and growth strategies. The transaction is expected to close in the second half of 2026.

- BASF Spin-Off.

BASF announced a restructuring effort in September 2024, carried out in 2025, that included plans to IPO its Agricultural Solutions business. The Agricultural Solutions business will focus on crop protection, seed and traits, and digital farming. Management believes the market has undervalued Agricultural Solutions. As of November 2025, BASF expects to list the new entity on the Frankfurt exchange by 2027 and retain majority ownership. The Agricultural Solutions business generated FY2024 revenues of $10.6B and adjusted EBITDA of $2.1B.

- Advanta IPO.

In September 2025, UPL, a major agrochemical company based in India, announced plans to list its seed subsidiary, Advanta Enterprises, on the Bombay stock exchange and National stock exchange. Advanta operates globally in over 80 countries, focusing on tropical and subtropical seeds for corn, sunflower, canola, and vegetables. UPL, along with minority stakeholder, KKR, expects the transaction to raise $500M at a $4B valuation, with UPL continuing to retain majority ownership. The listing is intended to allow the pure-play seed entity to be valued at a higher multiple and to operate with greater strategic focus.

- Syngenta IPO.

Syngenta Group, a Switzerland-based global seed and crop protection company, controlled by Chinese state-owned Sinochem, is considering plans for a $5B-$10B IPO for 10%-20% of its shares on the Hong Kong stock exchange during Q4 2026. Syngenta previously withdrew its proposed $9B listing on the Shanghai stock exchange. Proceeds are expected to support debt reduction, R&D and acquisitions. Syngenta Group generated FY2024 revenues of $28.8B and EBITDA of $3.9B.

- Corteva Separation.

Corporate transformations continue into 2026. FMC, a global crop protection company headquartered in Pennsylvania, announced in February an exploration of strategic options, including a potential sale of the company. We’ll keep track of the process throughout the year as major crop input companies explore corporate transactions.

2026 AGRONOMY OUTLOOK

Ag retailers may face rising operating costs and margin pressure in 2026. IT, insurance, and labor expenses continue to climb. Increasingly, digital tools are essential to compete. At the same time, ag retailer margins are compressing, because of the deteriorating financial health of crop producers (price sensitivity, reduced demand), rising competition from generics, technologies that reduce input demand and large growers bringing agronomy and application services in-house. These pressures are likely to reinforce ongoing consolidation in ag retail, especially for cooperatives. Some retailers prioritize operational efficiency by investing in larger, more centralized facilities rather than operating broad networks. Buyers now target operations that fit strategically within existing footprints and have winning characteristics, such as supply chain reliability, integrated solutions, differentiated product offerings, digital capabilities and employee talent depth.

Seed and biologicals producers will start consolidating. Seed companies continue to advance seed technology and development platforms, and larger players are likely to pursue acquisitions to secure leading genetics and maintain robust R&D pipelines. The biologicals market, still fragmented today, is poised for similar consolidation as suppliers seek to offer differentiated portfolios. Buyers are motivated both by the need to deliver superior products and by the growth potential of biologicals, which continue to capture share from traditional crop protection products.

The industry will continue reshaping itself around efficiency, scale, and innovative products and services. Ag retailers that can navigate cost pressures, invest in technology, grow strategically, build high-quality portfolios, and charge for valued services will prevail in a tough market.

Farrell Growth Group is a leading retail agronomy consulting firm with over 25 years of experience. FGG’s members represent over $5 billion in combined agronomy revenue and serve growers in 36 states as well as Canada. The firm has a strong track record in ag retail M&A, having worked on over 45 transactions.

Ocean Park is a leading boutique investment bank focused on industry segments across the agricultural supply chain including the ag inputs, ag retail, renewable fuels and chemicals, energy, food, and AgTech sectors. The Ocean Park team has significant operational and transaction experience, including advising mergers and acquisitions, financing and restructuring. Since its founding in 2004, Ocean Park has successfully completed over 90 transactions and client engagements, including over 40 biofuels transactions. Its office is in Edina, MN.

This material is solely for informational purposes. The information in this document does not constitute an offer to sell, or a solicitation of an offer to purchase, any security or to provide any investment advice. Any securities are offered through Ocean Park Securities, LLC, a member of FINRA and SIPC. Ocean Park’s professionals are licensed registered representatives of Ocean Park Securities, LLC. For more information, please visit oceanpk.com or call (310) 670-2093.